Most of the modern rise in the capital share is land, not capital

The much-discussed rise in capital's share of income is, on decomposition, overwhelmingly a rise in the value of land under housing — vindicating a core Georgist claim.

At a glance — When the modern rise in the capital share is decomposed, it is mostly rising housing — and therefore land — value rather than reproducible capital, a result independently replicated across US and European data. Evidence: Strong (independently replicated across US and European data) · 8 supporting sources · 2 challenging Strongest support: Rognlie (2015) — the long-run rise in the net capital share is concentrated in housing; ex-housing, capital's share is roughly flat. Strongest counter: Autor et al. (2020) — reads the falling labor share as a shift toward high-markup "superstar firms," capping how much the land story can claim.

The Claim

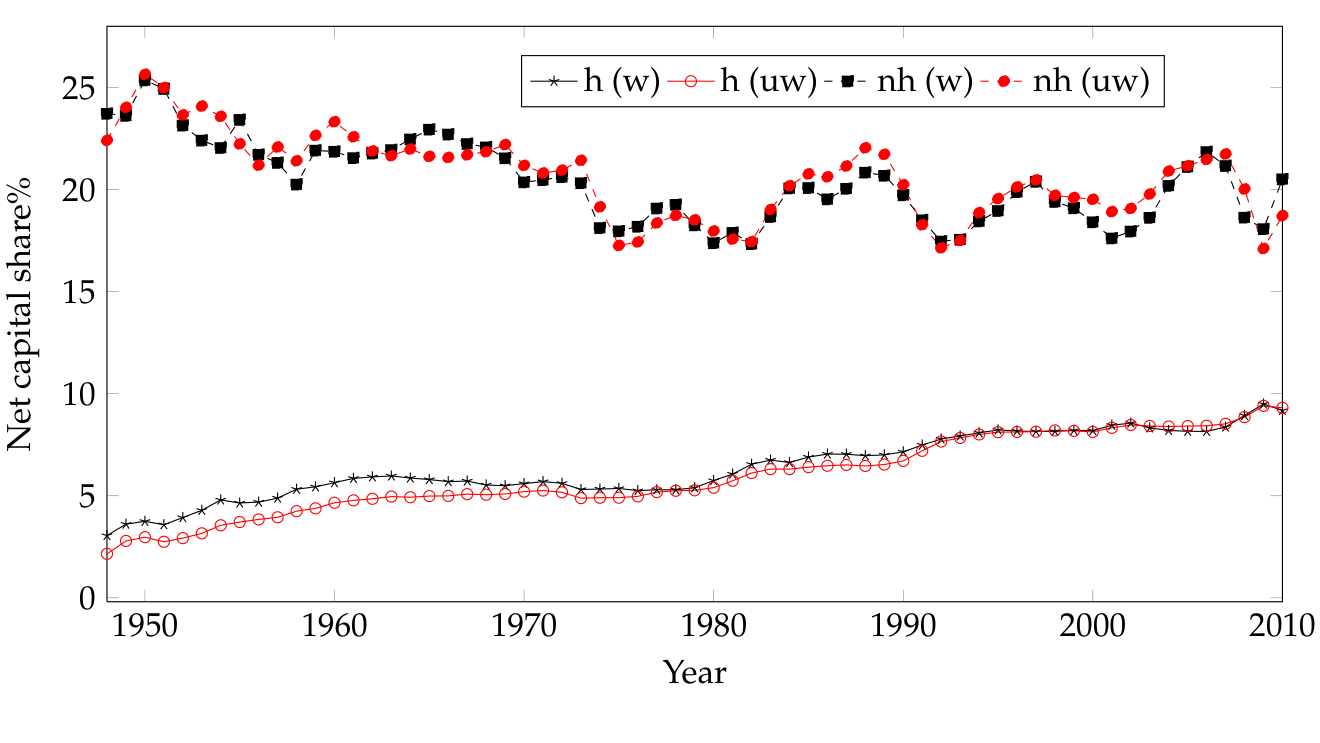

The rising share of national income flowing to "capital" in developed economies — popularised by Thomas Piketty's Capital in the Twenty-First Century — is, when decomposed, almost entirely a rise in the housing sector, and therefore largely a rise in land rent. Reproducible capital (machines, equipment, structures) shows little long-run increase in its income share; land does.

The Evidence in Numbers

| Study | Data | Finding |

|---|---|---|

| Rognlie (2015) | US + 7 advanced economies, postwar | The long-run rise in the net capital share is concentrated in housing; ex-housing, capital's share is roughly flat |

| Bonnet, Chapelle, Trannoy & Wasmer (2021) | French & European data | Rising wealth-to-income ratios are driven by land prices, not produced capital — independently confirming Rognlie |

The two teams used different countries and methods and reached the same conclusion: the "capital" in rising capital shares is mostly location. Three further studies fill in the chain. Knoll, Schularick & Steger (2017) supply the price history behind it: across 14 advanced economies, real house prices were roughly flat for eight decades and then rose sharply after 1950 — a boom the authors attribute mostly to rising land prices, not construction costs. La Cava (2016) traces the income side for the US: the postwar rise in housing's share of income is overwhelmingly imputed rent to owner-occupiers, concentrated in supply-constrained states — a land-scarcity story down to the state level. And Furman & Orszag (2015) connect the housing channel to the wider rents debate, flagging land-use-driven housing rents as a contributor while locating much of rising inequality in skewed firm-level returns.

The Counter-Evidence — the Firm-Rents Reading

The honest counterweight comes from the firm-level literature, wired here as challenged_by. Autor, Dorn, Katz, Patterson & Van Reenen (2020) explain the falling labor share without land at all: reallocation toward high-markup "superstar firms", read substantially as an efficiency story. Barkai (2020) measures a fall in both the labor share and the required-return capital share in US nonfinancial corporations since the 1980s, offset by rising pure profits attributed to market power, not land. Neither paper rebuts the housing decomposition directly — they work on different data at a different level — but both cap how much of the economy-wide shift away from labor the land story can claim for itself. The wiki's corporate-rents outcome carries that side of the ledger in full.

A Georgist Ancestor-Statement (1991)

The decomposition above is a modern, quantitative finding, but the underlying claim — that what U.S. tax and national-accounts data call "capital" gains and capital income are, on inspection, mostly land gains — is not new. Mason Gaffney (1991) made essentially the same argument a quarter-century before Rognlie's decomposition, using tax-code evidence rather than macro data: he catalogued the U.S. income tax's extensive preferential treatment of "capital gains" — deferral, covert land depreciation, step-up of basis at death — and argued these provisions overwhelmingly benefit land rather than produced capital, because true capital "depreciate[s], usually fast," while land's "gains" are pure, undiminished appreciation. This is listed here as the argument's Georgist ancestor-statement, not as independent quantitative confirmation of Rognlie's or Bonnet et al.'s specific magnitudes — Gaffney's essay is advocacy reasoning from tax-code mechanics and anecdote, not a national-accounts decomposition. See the full page for its honest limits.

Why It Matters

If inequality's capital dimension is really a land dimension, a tax on land values targets the actual driver — without the efficiency cost of taxing productive capital. This connects 21st-century inequality research directly to Henry George's 19th-century diagnosis in Progress and Poverty.

A further confirmation arrives from the factor-share side. Kerspien, Madsen & Strulik (2025, European Economic Review), using annual data for 16 advanced economies over two centuries, find the post-1980 decline in the labour share is driven "not by the overall quantity of capital, but by its changing composition" — above all the rising real price of buildings — reinforcing the reading that the shift away from labour is a real-estate phenomenon rather than an equipment one. (They frame the appreciating asset as "buildings" and leave the land-versus-structure split to the house-price literature, so the "buildings are land" step is supplied by Knoll et al., not by this paper.)

Strength of Evidence

Strong — independently replicated across US and European datasets by separate research teams.

An independent macro confirmation comes from Bakker (2023, IMF): standard growth decompositions overstate capital's contribution by "failing to account for the substantial part of capital income directed to urban land rents" — recorded capital income is partly land rent, which is this claim stated from the measurement side.

Further corroboration. Rognlie's 2014 note first showed the net-capital-share rise is concentrated in housing and land, and that diminishing returns to capital undercut Piketty's mechanical rising-share logic. Stiglitz (2015) reaches the same conclusion from theory: most of the rising wealth-to-income ratio reflects rising land values, not productive capital. Davis & Heathcote's Fed-affiliated series shows residential land's share of housing value rising to 46% by 2006, with land prices roughly three times more volatile than structures.

See Also

- McKinsey Global Institute (2021): The Rise and Rise of the Global Balance Sheet — mainstream institutional balance-sheet evidence that real estate dominates global net worth, corroborating the land-share-of-wealth story from outside the academic capital-share literature

- Blanco, Bauluz & Martínez-Toledano (2018), Wealth in Spain 1900-2014 — a national case study (Spain) extending the land-decomposition finding to a country where land's share of wealth is unusually pronounced

- Hornbeck & Moretti: who benefits from productivity growth — "the split between labor and land is potentially more consequential... than the split between labor and capital"

- Kerspien, Madsen & Strulik (2025): Capital Composition and the Decline of the Labor Share — 16-country, two-century evidence that the labour-share decline tracks rising real building prices, not the quantity of reproducible capital

- Piketty, Capital in the Twenty-First Century — the dataset the land decomposition reinterprets (context source)

- Economic Rent · Unearned Increment · Land Value Tax

Sources

- Matthew Rognlie (2015), "Deciphering the Fall and Rise in the Net Capital Share," Brookings Papers on Economic Activity — used for the finding that the long-run rise in the net capital share is concentrated in housing/land, not reproducible capital. wiki summary · PDF

- Bonnet, Chapelle, Trannoy & Wasmer (2021), "Land is Back, It Should Be Taxed, It Can Be Taxed," European Economic Review — used for the independent European replication decomposing capital into land vs structures. wiki summary · PDF

- Mason Gaffney (1991), "'Capital' Gains and the Future of Free Enterprise" — used, as an attributed 1991 Georgist ancestor-statement rather than quantitative evidence, for the tax-code-level argument that preferential capital-gains treatment overwhelmingly benefits land rather than produced capital. wiki summary · PDF