Originally published on Progress and Poverty on September 24, 2025. Republished on Progress.org with permission.

Across the country, cities and states have built a patchwork of property-tax abatements that creates hidden incentives, favoring some groups over others. Each year brings another exemption, a longer abatement, or a special “in-lieu” arrangement negotiated behind closed doors. The result is a system that is hard to track, easy to game, and riddled with inefficiencies.

The Lincoln Institute of Land Policy estimates that local governments forgo $5 to $10 billion each year from business property-tax incentives alone. And that is before we even reach the homeowner credits and homestead exemptions that usually dominate the conversation.

This article is not about those homeowner programs. It is about the other, less visible property-tax structures that quietly reallocate billions of dollars. These are the deals and classifications that shape whether cities encourage apartments or offices, retail or vacant lots, investment or disinvestment.

Over the past year, I have explored and modeled many of these systems, so I want to tell some of those stories. Over many places, I have found an implicit acknowledgement by local governments that the current property tax is flawed. In analyzing this web of distortions and carve-outs, I observe that many of them rely on principles which, if taken to their logical conclusion, point clearly towards shifting tax burden from buildings to land. Yet instead of fixing it, they have created a work-around culture of exemptions and carve-outs that privilege the well-connected and lock in inefficiency.

Deal‑by‑Deal Governance

Case 1: If Baltimore builds it, will they come?

If you want to see the anatomy of a modern tax deal, go to Baltimore’s south shoreline. A decade ago, the Port Covington team pitched a city-within-a-city: new headquarters, offices, housing, streets, parks, and a waterfront stitched back together. To make it pencil, they asked for what became the largest financing package in city history, $660 million in tax-increment bonds, backed by future property taxes inside the district.

What’s a TIF?

Tax-increment financing (TIF) is a local mechanism to pay for roads, sewers, and other public works for new developments. In a TIF, the city pays for these up front by having others pay (bond) under the promise the city will pay the money back. They pay the money back by reserving the increased property taxes from the new development over the next 30 years to pay off the bonds. And if the project fails? The city is subsidizing and buying into the risk.

In Baltimore, the City Council approved the Port Covington TIF proposal while the project also stacked several other property tax abatements as well as Opportunity Zone funds. The proposal was a high-gloss vision that depended on pulling tomorrow’s tax base forward today.

As the project moved ahead and rebranded as “Baltimore Peninsula,” a different picture emerged: sleek new buildings and fresh pavement, but eerily empty blocks. A viral “ghost town” video captured what residents felt on the ground: the public had paid dearly up front, while the promised density lagged behind. Whether the district matures into what was promised is still uncertain. What is clear is how the deal was assembled: project by project, meeting by meeting, with extraordinary fiscal commitments that will shape the city’s balance sheet for decades.

Case 2: Hackensack’s Handshake Exemptions

The same choreography plays out elsewhere, just with a different cast. In Hackensack, New Jersey, the outgoing council rushed through several long-term tax-exemption agreements right after the May election, including two 30-year PILOTs and a 15-year PILOT.

What’s a PILOT?

A PILOT, or “payment in lieu of taxes,” is basically a side deal between a developer and a city. Instead of paying the normal property tax bill, the developer makes a negotiated payment, usually smaller or phased in over time. Cities like them because they can nudge projects that might not pencil otherwise. Developers like them because the payments are predictable and often much lighter than the standard tax.

The gamble is obvious. If the project does well, the developer locks in a tax break their neighbors don’t get. If it flops, the city has already given away the revenue.

In Hackensack, one of the biggest deals was One Essex, a $107 million, seven-story development with 250 apartments and a 435-space garage. It was granted a 30-year PILOT in June. Within weeks, the new council moved to rescind several of the rushed agreements, triggering litigation. This is the politics playing out all across the country, often hiding from the public eye. Whether you support or oppose the projects, the process tells the story of high-stakes fiscal commitments negotiated for a handful of parcels, hidden inside local politics.

Case 3: South Bend’s One-Parcel Areas

In South Bend, Indiana, the Common Council recently approved a property-tax abatement tied to a new 50-unit affordable apartment building planned for the vacant corner of South Main and Donald Streets, an incentive structured around the project’s new construction and granted under Indiana’s Economic Revitalization Area (ERA) statute, which authorizes local “designating bodies” to declare ERAs and award real-property improvement deductions by resolution.

On paper, the law allows a city to map neighborhood-scale ERAs covering up to 10 percent of its total land. In practice, South Bend usually takes a narrower path: it draws the boundaries around a single parcel, treating one lot as an economic revitalization “area.”

The result is a city where incentives are not broad-based, but negotiated case by case. To build with tax relief in South Bend, a developer must be prepared to navigate the politics, hearings, and handshakes required to get the council on board for one specific site. This is precisely the type of ad hoc policymaking that is ripe for corruption & backdoor deals.

I am not alleging outright foul play in any of these examples. Many of these projects are pursued with good intentions and real community benefits in mind. But even when corruption is not present, the structure itself is corrupting. It creates a system where access and privilege determine who gets the break, and where rules are bent to fit the deal. At minimum, it is a process reserved for the well-connected.

And when you zoom out from individual deals, the bigger picture is just as troubling. Cities like Baltimore show what happens when the patchwork of carve-outs piles up over time: a sprawling lattice of exemptions layered on top of one another, held together with political glue rather than clear rules.

Case 5: Baltimore’s Many Bandaids

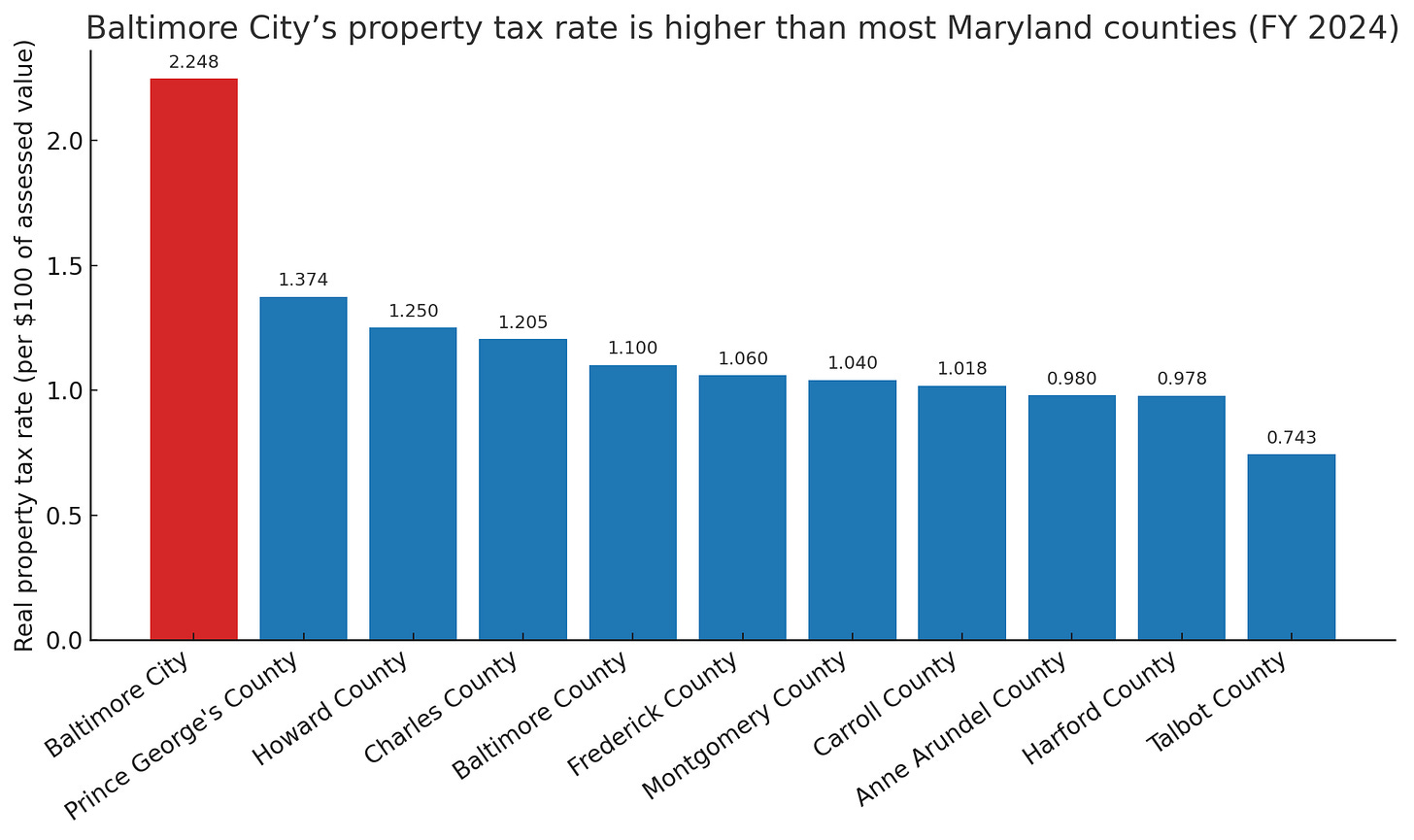

Baltimore is the clearest case study of a sprawling lattice of exemptions. The city’s base property-tax rate is 2.248 percent, almost double anywhere else in Maryland. To soften the blow of that high rate in a city struggling with vacancy and disinvestment, Baltimore has built an elaborate web of tax breaks: historic-rehabilitation credits, multiple “high-performance” housing credits, enterprise-zone benefits, home-improvement and targeted homeowner credits, and more. On top of these sit the bespoke instruments like TIFs and PILOTs.

The city’s own budget office took a hard look at this portfolio and, in a comprehensive review, tallied $126.7 million in tax credits with recommendations to cap, rationalize, and better target what had become a broad, expensive set of carve-outs. Baltimore’s patchwork is not a strategy, it is a workaround to paper over the contradictions of a property-tax system that punishes investment and then tries to claw back exemptions to encourage it.

Case 6: Hidden Incentives in NYC and Colorado

The complexity is not just in individual deals. In many states, the very structure of the property-tax code favors small-scale, owner-occupied housing while putting heavier burdens on apartments, commercial buildings, and other larger developments. These rules are not exemptions you apply for, but classifications built into the system itself.

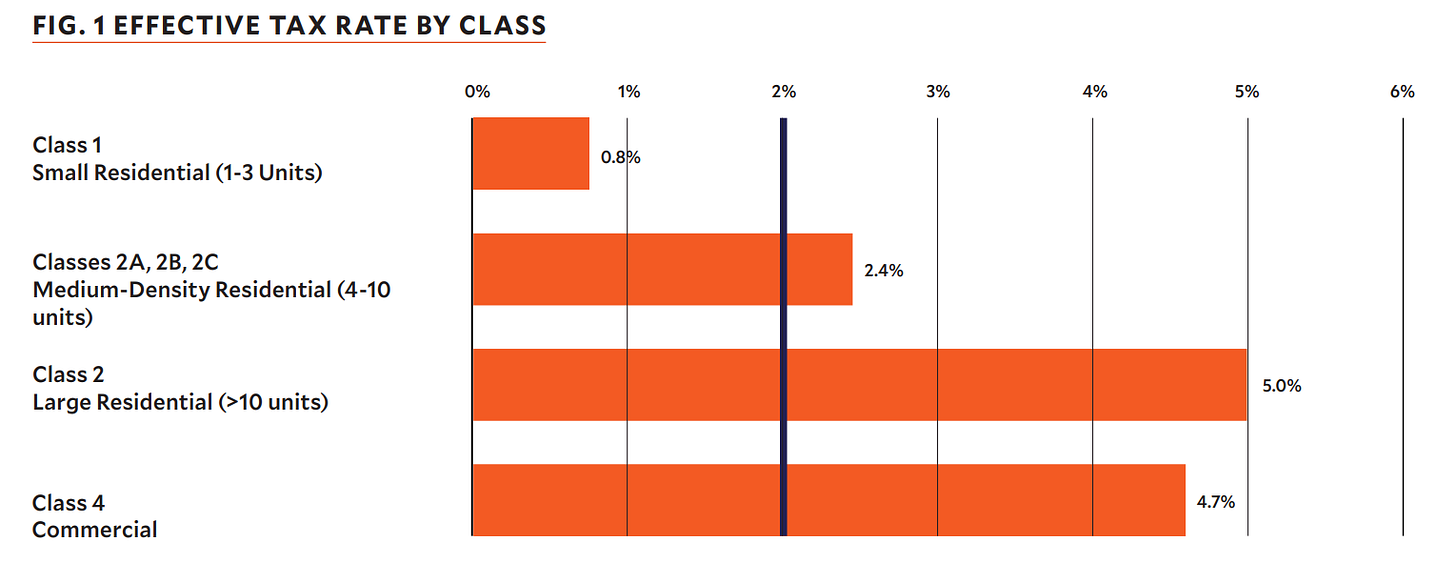

Take New York City’s property-tax system which divides the world into four classes. Class 1 is mostly one- to three-family homes; Class 2 is multifamily rentals, co-ops, and condos; Class 3 is utilities; Class 4 is commercial. NYC then uses complicated mechanics that ultimately push a disproportionate burden onto rentals. Long-standing valuation rules for co-ops and condos, class-share constraints, and targeted abatements combine to make many owner-occupied apartments and single-family homes undertaxed relative to their market value, while large rental buildings bear higher effective tax rates that landlords pass through to tenants. In practice, this system places an outsized load onto low-income renters compared to wealthy homeowners while also tilting development incentives against commercial uses.

Colorado tells a similar story. After assessing the full market value of property in the state, Colorado reduces the taxable value based on the class of property. Residential property is assessed at around 7%, meaning a $100,000 home is only taxed on around $7,000 worth of value. Meanwhile, most nonresidential property is assessed at 27% of market value… almost four times as much.

That is a structural, statewide tilt: the same dollar of commercial value turns into more than four times the taxable base as a dollar of residential value, before a single local mill is applied. The politics of that tilt are complicated; the economics are not. It discourages investment in the very places—mixed-use buildings, neighborhood retail, light industrial—where cities need reinvestment most, and it pushes jurisdictions toward the same menu of bespoke exemptions and abatements to counteract the very burden the state’s math created.

Throughout our property tax system, we are crafting winners and losers under the recognition that property taxes determine incentives.

The Endgame: Exempt Buildings, Tax Land

Cities didn’t arrive at this patchwork by accident. Piece by piece, they’ve implicitly recognized three truths about regular property taxes.

- The property tax behaves like two different taxes: one on what you build (the building tax) and one on where you build (the land tax).

- Taxing buildings is counterproductive.

That’s why modern economic development tools routinely wipe out taxes on improvements like new‑construction abatements and rehab credits aimed squarely at the building, not the dirt. - Development raises land values and urban resilience.

This is the premise of TIF funds. No “increment” exists to bond unless projects lift land and property values.

Cities explicitly know that property taxes shape incentives. If they started to explicitly recognize the three truths, the endgame writes itself. Stop taxing the thing you want more of–buildings–and acknowledge that the stable, community-created value resides in land. Replace the ad hoc carve-outs, the bargaining, and the quiet favoritism with a simple rule that aligns private incentives with public goals.

Exempt buildings universally. A universal building exemption would unwind the quiet corruption of parcel-by-parcel negotiations, and make room for the broad-based, incremental improvements that actually make cities thrive.

Greg Miller is the President of the Center for Land Economics.