Originally published on Progress and Poverty on April 28, 2026. Republished on Progress.org with permission.

This is the latest article in the “Mass appraisal for the masses” series, based on an interview with Thomas Holding, an assessor from North Carolina I met at the 2025 IAAO Annual Conference in Orlando, Florida.

Among other topics, this series previously covered the early 20th century communal system for valuing land, the simplest viable method for valuing land, and how South Korea values land.

Today’s interview turns its focus back to the US, describing the most common and established methods for valuing land that are actually in practice in property tax valuation offices throughout the United States.

NOTE: Neither the Center for Land Economics nor Progress & Poverty Substack has any business relationship with Thomas Holding and his employer, Piner Appraisal.

Thomas’ Background

LARS: Tell us about yourself, Thomas.

THOMAS: I’m a certified general appraiser in the state of North Carolina. I have a background not just in fee appraisal1, but for the last decade or so, I have also worked in tax offices2 as an appraiser in both the commercial and residential sides. Before that I worked with clients—typically law firms—that would hire our appraisal firm when contesting their client’s assessed valuations. Typically, these were commercial or industrial type properties.

LARS: Is it safe to say you’ve been on all sides of the aisle? “Defense” and “prosecution,” fee appraisal and mass appraisal, public and private sector?

THOMAS: Very safe to say. Correct.

LARS: And you’re with a company now, Piner?

THOMAS: Yes, Piner Appraisal, which has three separate entities, each offering different services related to mass appraisal. We have an imagery division, solutions division, and then we have a software division. At Piner Appraisal, we concentrate on doing mass appraisal for different counties, principally in North Carolina.

LARS: How many years of experience?

THOMAS: Total, around 30 years, in fee and mass appraisal. I’ve been an employee in three different county tax offices, all in North Carolina. They ranged from a relatively small county all the way to one of the largest counties in the state, which was Wake County.

LARS: How many parcels are in Wake County?

THOMAS: I believe there are around 430,000 now. When I was there, they were in the 350,000 range, but it is growing exponentially.

LARS: And what’s the smallest you’ve done?

THOMAS: 65,000.

LARS: So you’ve done all scales, you’ve done private, you’ve done public, you’ve done government, you’ve done not-in-government, you’ve done fee appraisal, you’ve done mass appraisal. What about sectors? Have you done residential, commercial, etc.? What sides of it have you done?

THOMAS: All of it. When I started out, I was working under the tutelage of a fee appraiser, and his specialty was in property tax assessments, challenging the valuations. Principally, that was for large commercial clients and it lasted for nine years. After that I began my governmental career working at two smaller county tax offices before moving back to Raleigh and working for Wake County. No matter the tax office, they all start you out measuring decks, working permits, and picking up new construction. In Wake County, they eventually let me work on commercial appeals.

LARS: So would it be safe to say you’ve pretty much seen it all?

THOMAS: I’ve seen a lot.

The Sales-Adjusted Cost Approach

LARS: What is the basic valuation procedure used in tax offices?

THOMAS: Ultimately, when you break down what we do in a tax office, everything is separated out between the improvements and the land. The way it is, in North Carolina at least, everything is on a cost basis.

LARS: Let’s have a quick term definition. You just said “cost basis.” By “cost,” you mean the replacement cost of the building?

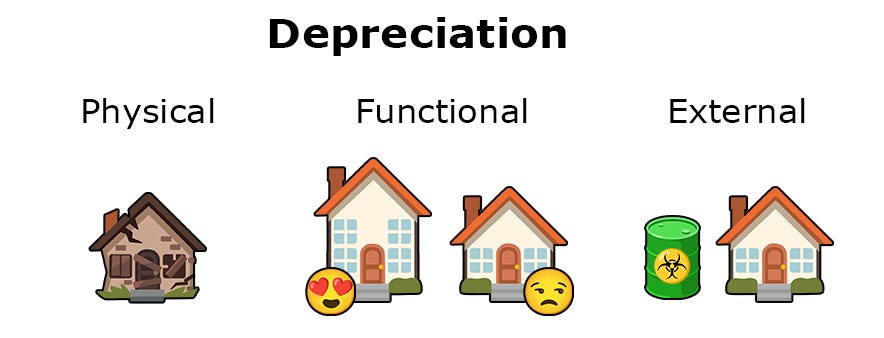

THOMAS: Yes. Ultimately, you’re looking at the cost of construction; cost to construct, minus all forms of depreciation—physical, functional, and economic.

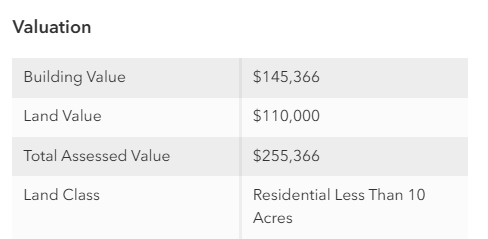

LARS: There’s three lines in your final appraisal, right? There’s your total market value, there’s your land value, and there’s your improvement value, right?

THOMAS: Correct. Because the cost is worked out in advance of valuing the land, ultimately, once you set your cost schedules, really all we’re valuing is the land.

Cost Schedules

LARS: Interesting. So you say the “cost schedules” are frozen ahead of time. Is that a North Carolina thing?

THOMAS: It might be. I know for each county in North Carolina, when you set your cost schedules for the different building types and different things, that has to be voted on and approved by the county commissioners. And there’s a public hearing too. So in theory, anybody from the public can go in there and can contest those costs.

LARS: So those cost schedules, those are all public. Can anyone get to see those?

THOMAS: Yes.

EDITOR: Here’s the Wake County, NC 2024 schedule of values.

LARS: That’s very interesting. So you’re saying in North Carolina, they’ve decided as a matter of law, that they go get the best evidence they can, gather all this construction information, then freeze it so they’re limiting the assessor’s degrees of freedom?

THOMAS: It can be limiting, however it’s not meant to straitjacket assessors. In order to comply with state tax laws, and provide ample time for local government and public input, there has to be a cut off point so that the rest of the revaluation process can proceed.

LARS: So if you’ve got this kind of a building, these are the cost books you have to use.

THOMAS: Correct.

LARS: And then you said something interesting. You said, “really all we’re valuing is the land.”

THOMAS: In a way, yes.

LARS: You’ve got these cost books you have to use, and those are frozen ahead of time. So elaborate how you get from there to the final value.

THOMAS: So in theory, if the depreciated cost of the components has been determined by your modeling in the CAMA3 system, the only unknown variable is the land value.

LARS: So when we say “replacement costs,” we mean “what would it cost if I had to replace my house today?” But then you have to subtract from that cost the other word you used, “depreciation.” Let’s tackle that first.

Depreciation

THOMAS: Correct. If you were to build it as of today, you’ve got a brand new house.

LARS: But the depreciation is—my house has had three children and one cat in 15 years. So wear and tear?

THOMAS: Well, there are various forms of depreciation. There’s functional depreciation, then there is the physical age of it.

LARS: But say, crayons on the walls? Holes in the roof? That’s physical, not functional?

THOMAS: That’s physical.

THOMAS: For functional depreciation, say you have a three bedroom brick ranch with one bathroom. In a modern marketplace, most families want a house with at least two bathrooms. You would have to sell for a reduced price, because it’s a disincentive to the market for you not having that extra bath.

LARS: So an extreme example could be that I built a ski lodge, but then all of a sudden, because the Earth’s axis shifts or something, the weather changes and now it’s at the beach. There’s not much demand for a ski lodge at the beach?

THOMAS: Now that’s what we call an external obsolescence, which is another kind of depreciation. It’s kind of like if you build a subdivision next to a garbage dump, and there’s a nasty odor throughout the neighborhood due to its proximity to the landfill. That is an external factor you cannot control. But that is a type of an externality that you have to adjust for that affects value.

LARS: Or if I have a lake house and then the lake dries up?

THOMAS: Right. It’s no longer a lake house. That’s external. Functional depreciation is to the house itself. If the typical expectation in the market is two and a half baths and your house only has one bath, but the market wants two baths at a minimum, you’re going to have to sell that house at a depreciated value relative to the rest of the houses in the market. Because that’s a market expectation. Now you have to determine the “cost to cure.” The cost to cure is to build another bathroom. Is the cost to cure or remedy that functional obsolescence greater than the cost that you’re going to receive in the market?

LARS: Okay, so let’s lay that out. The different kinds of depreciation you mentioned: physical, functional, and external.

LARS: Do all of them have a cost to cure?

THOMAS: No, you might have to judge. You can’t cost-to-cure an external one, unless you move that whole subdivision away from the garbage dump or maybe close the dump down. You can’t cure the fact that the lake dried up, but you can cure functional obsolescence by adding a new bath, if it makes economic sense.

LARS: Or replacing the roof.

THOMAS: Well, that’s more physical than functional. You’re lessening physical depreciation by putting on a new roof and extending its physical and possibly economic lifespan. As an appraiser, you’re not really looking at how long the building will physically last, you’re looking at how long the improvement will continue to add value to the parcel. This is typically determined by the market, and is referred to as a structure’s remaining economic life. When added together, if all of the forms of depreciation exceed the current depreciated cost of the improvement, then that structure will have no contributory value. If it can’t be cured by correcting the functional obsolescence and physical condition, then that improvement will have reached the end of it’s economic life. When the improvements no longer contribute to the overall value of the property, this could also be an indicator that the highest and best use might be changing to an alternate use.

LARS: So if the highest and best use here used to be, I don’t know, a fishing shack, but now it’s a big subdivision or whatever?

THOMAS: It might be, if the site is large enough, it might go from commercial to residential, or as is typical in many urban areas, a residential neighborhood might be changing to commercial.

LARS: So for example, this used to be just a little house on the prairie, but now it’s a happening business center, and highest and best use might be that we should put a three-story office building here?

THOMAS: Correct.

LARS: So first, you’ve frozen these cost tables. Then there’s the cost-to-replace-new, but then there’s also these three forms of depreciation and obsolescence to worry about. Now are those depreciation tables frozen as well, or are they specified in mechanical guidelines you must follow?

THOMAS: They are approved and set when the schedule of values is approved. Depreciation tables are meant to recreate typical economic life cycles of different property types and should represent local market norms as much as possible during a revaluation period. After testing, depreciation tables are submitted to the representative taxing board or county commissioners and are voted on as well. If approved, they are used in property analysis and do not change. As I stated before, because everything has to be presented to the county commissioners and public, there has to be a cut off point so that the rest of the revaluation process can proceed.

LARS: And so from a kind of devil’s advocate perspective, right or wrong, you don’t have a choice, but to follow those rules once they’re voted on.

THOMAS: Once they’re set, yes.

LARS: And so if there’s a problem with them, then the cure is to make better decisions before you vote on them.

THOMAS: You don’t typically have a problem with the cost or depreciation tables. Before you submit them they have been pretty thoroughly tested.

LARS: But generally speaking, are they pretty good?

THOMAS: You can get very close when modeling your cost and depreciation schedules. The IAAO has many great courses that teach how to do all these things.

Land Residual Theory

LARS: Let’s say a property sells for something that does not match the simple cost to replace it in the abstract. Is the difference typically just the land value? According to the naïve “land residual” theory at least? Or is there more to it?

THOMAS: No, not necessarily.

LARS: Let’s go into that.

THOMAS: In appraisal theory, like I said, you have three approaches to value. We have the sales comparison and cost approaches, where you analyze sales prices and the cost to build (including the land and site costs). If you have an income component, there’s also the income approach. In theory, all three methods should arrive at the same value, unless there is an imbalance in the Four Factors of Production4. Land residual theory is more of an appraisal/economic concept that says land value is what remains after the other factors of production have been paid. Under land residual theory, the income generated by the property is first allocated to non-land components like the building and the business. Whatever income is left over is attributed to the land and is then capitalized into an indication of land value.

LARS: You just listed the “cost approach” and “sales comparison” approaches as two separate things, but appraisers I talk to often say they use the “sales-adjusted cost approach.” Is that a hybrid of the sales comparison approach and cost approach together, or is it a separate term of art?

THOMAS: A sales-adjusted cost approach is best understood as a cost approach calibrated by market sales, not as a separate third approach and not exactly a full hybrid approach in the same sense as blending two independent indications of value. In assessment work, especially mass appraisal, we often build cost schedules for structures, and depreciation tables for age, condition, and quality. But those schedules cannot simply be theoretical construction-cost numbers. They have to be tested against actual market behavior.

LARS: So you’re doing a cost approach and then you’re also looking at the market sales and reconciling them?

THOMAS: Yes, in a way. That is where the “sales-adjusted” part comes in. After developing the cost model, the model is checked against qualified sales. If the model is consistently too high or too low for a neighborhood, property class, age group, market area, or building type, market-derived adjustments or calibration factors can be applied if necessary. Those adjustments are derived from sales, but the underlying valuation framework is still the cost approach. There are always things in real estate markets that are hard to gauge, and you know, the standard variations in sale price you’ll typically see out in the wild for residential housing is between 5 and 8%. These are just normal market variations. People have their preferences like, “Hey, I like that kitchen better…”

LARS: “There was a peach tree in the backyard that reminded me of my mom.”

THOMAS: Exactly. And I’m paying more.

LARS: And someone else is a hard bargain driver. And so you’ve got that central tendency that runs through it and then some people get a good deal, some people get a bad deal, some people get nostalgic.

THOMAS: But to them, it might not be a bad deal because they wanted whatever feature that was.

LARS: Do you just follow that central tendency of the market rather than any individual sale?

THOMAS: Yes, we’re reacting to where the market is going and then we’re trying to model that as best as you can within the constraints of our CAMA system.

LARS: And the market is more an overall tendency than anything reflected in any individual sale?

THOMAS: Yes.

LARS: So my next question is, now that we’ve done all the homework and explained to the lay audience, what all our jargon and our terms mean and what we’re working with and how we’re limited by the cost tables, at least in North Carolina, how do you then make up the difference and create a combined value, a full, filled out, all three lines that matches the market tendency that you’re seeing and is also well supported and defendable? How do you do that?

Location, Location, Location

THOMAS: It’s not just as simple as the remainder is the land value, because there could be other elements. It could be an external factor like we talked about that is affecting that particular property or a group of properties. They could be next to a garbage dump. So that might require a local adjustment made just for that specific neighborhood. Those houses might be tract houses in this neighborhood that are exactly the same as tract houses across the county made by the same builder and everything. But just because of an external factor that affects this group of houses, we might have to apply some type of factor to make them reflect the market in that particular neighborhood. It’s locational in effect. It’s located next to a dump. It’s hyper-local. It’s an external factor that affects that. So that’s some assessor jargon.

LARS: So an “external factor” is something that might apply to a very specific localized area as opposed to a land table for a whole area?

THOMAS: Correct. The general model should match the greatest number of parcels county wide. Then you drill down into the ones that don’t fit on the line. The hardest part to appraise is not the properties that fit the model. We spend the most time generally in looking for the ones that don’t fit and try to determine “why didn’t it fit?” Is there some factor that I have overlooked that might be affecting its value that I need to compensate for in some way?

LARS: So you’re examining the market for those factors. So you do not just do a one-size-fits-all solution? You might start with a broad brush, but then you notice that you have to dial in these exceptions?

THOMAS: Correct.

LARS: And what are those exceptions?

THOMAS: All the typical ones that apply to real estate like location, size, age, condition, quality, extra features, and economic or market conditions. A locational factor could be how close a property is to a metro station. That might be a positive factor, but if the residential property is located directly adjacent to the rail line and is subject to loud noises 24/7, then to some people this might be a negative factor. If this is reflected in the sales data of properties that have these attributes, as opposed to properties that do not suffer from the same condition, then you can usually derive a suitable adjustment factor that can be applied to those specific properties.

Land Value and Size

LARS: It sounds like you start with these cost tables, and then you also have sale prices from the market. The prices tell you where the general market tendency for an area is for a certain kind of property. But each property is unique, and has unique characteristics. You punch those characteristics into the cost tables, and you get your cost value plus depreciation, and you work out your functional depreciation and all the rest of it. And then, you have land values that you can paint across a neighborhood. However, lots can be different sizes, they can be different shapes. How do you handle that? Does each lot get a standard base value with exceptions, is it handled per square foot, per acre, how do you do it?

THOMAS: Different tax offices do it in different ways. Particularly in tract neighborhoods, they might have assigned a base lot value, which is standard for every lot in that development regardless of size. Usually the unit of measure for the land depends on several factors like its size, shape, or maybe road frontage. For residential neighborhoods, typically the lot value is used.

LARS: So within a neighborhood, the same price per lot.

THOMAS: Correct.

LARS: And is that to reflect a market where people are like, “I don’t really care how big the lot is as long as it’s big enough for a house?”

THOMAS: It might. And you tend to find that in urban areas everything’s generally a rectangle or a square, there’s not even that much of a change in size anyway.

THOMAS: You might find more variation in rural areas, or you’ll see parcels around a cul-de-sac that are pie or more wedge shaped and are larger than a typical parcel in the same development. You might have two residential parcels and one is a standard size, and one might be twice that size. But they’re zoned the same, they have the same utility, the same use. When compared to the smaller average sized parcel, the larger parcel has “extra” land. That “extra” land has to be evaluated, so as an appraiser, you have to perform a series of tests to determine what value if any the extra land adds to the overall value. You can look at the zoning to see what you can legally do to that extra land. Can it be separated from the main tract and developed on its own? If it can pass a series of tests, the appraiser can determine if the “extra” land is excess land or surplus land. This applies to both residential and commercial properties. If a larger parcel can be subdivided, then you will have to determine the highest and best use of the hypothetical parcel.

LARS: So when you say “highest and best use,” you’re really saying “highest and best legal use?”

THOMAS: That’s part of it. It might be a physical use too. If the parcel’s half an acre, it might be zoned for that, but if you can’t physically put another structure there, it’s not physically possible to do it. Land has to pass all these tests: is it physically possible, legally permissible, is it financially feasible and will it generate the highest return to the owner?

Excess Land vs. Surplus Land

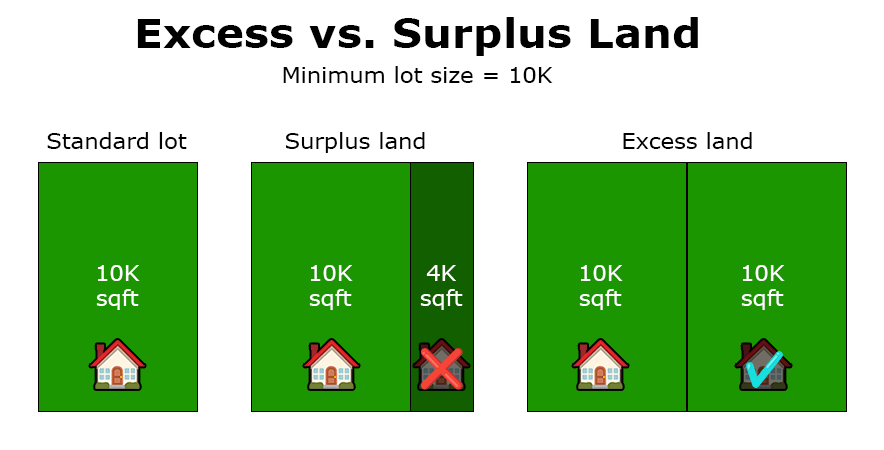

LARS: You just used some terms I’d like you to define for our audience: “excess land” and “surplus land.” What is the difference?

THOMAS: Surplus land is extra land that is not currently needed to support an existing improvement, and that land cannot be separated from that parcel and have another use. Say you have zoning that’s a minimum lot size of 10,000 square feet. If you have another lot next door that’s 14,000 square feet, you can’t chop off 10,000 for one house and 4,000 for another and legally build another house on it. The 4,000 square foot portion really doesn’t have the same functionality as the other. You can’t split it off, you can’t redevelop it and put another house on it. It’s just extra undevelopable land that typically has little contributory value relative to the base lot.

LARS: I believe the way you put it yesterday was: “surplus land is just more grass to mow, but excess land is extra land you have that you could, if you wanted to, turn into its own lot or its own use.”

THOMAS: If it passes all the tests I previously mentioned, there’s a potential that’s not being met and you can develop it for a separate use. This is why surplus land is more valuable.

LARS: And you’re making those designations in the CAMA?

THOMAS: It depends on the system. In different counties where I’ve worked, that might not be noted in the parcel information. If you can visualize the parcel characteristics like size, shape, topography and zoning when you’re looking at ArcGIS or aerial photography, you usually get an indication that a parcel needs to be looked at a little more. If it’s necessary, you can always determine the value of the excess land and apply that as some type of adjustment.

How Complicated is it?

LARS: There’s this phenomenon when anything you know how to do feels easy to you, but to someone who doesn’t, it feels impossible. When I talk to people about valuing land, they sometimes say, “it’s going to be so insanely complicated, we’re going to have to hire all these people to do it. Meanwhile, I see we’ve got, what, 11,000 property jurisdictions in North America, and the staff are already there and their salaries are already being paid? There’s someone local who’s already doing it. And in your jurisdiction, that person was you. Is this actually as complicated as it sounds?

THOMAS: Not really. I found in working with the public, a lot of times the hardest part is just explaining things to property owners. “Why is my value different from my next-door neighbors?” or why, especially in commercial, are there different grades or condition ratings? As far as valuation, once you understand it, appraisal theory is appraisal theory as long as you can recognize those factors that affect the value. I guess sometimes the hardest part is recognizing those factors but a lot of that just comes with experience.

LARS: I guess people just get intimidated by the fact that there’s so many parcels that no one could possibly ever do it in a year.

THOMAS: That is difficult. If you notice in most tax offices, when you’re looking at the records going back and you see adjustments in the system for size and shape, and topography. Those usually go back many years because a lot of those factors don’t really change unless the parcel geometry changes due to a sale or a split or something like that. In CAMA systems, that data has been accumulated over many revaluation periods and so that’s why we don’t just discount it and start with a clean slate each time because generally there’s not enough staff, resources or time to individually inspect every single parcel.

Land Appraisal 101

LARS: Okay, now, break it down for me for the sake of our audience. Let’s say I’m a junior appraiser, you’re the chief appraiser, and you tell me “Lars, we’re putting together an in-house land team, you’re the apprentice, here’s a neighborhood and you’re going to value all the land in it. Here’s all your ingredients.” Lay it out for me, how do I do it? Starting with the basics and then building up little by little?

THOMAS: If you’re starting out, you’re going to have them evaluate a tract subdivision where everything is cookie-cutter, as much as possible. That’s a great way to learn, because you can see very clearly the breakout of the costs. A lot of times you go into a subdivision by a tract builder like Lennar, or one of the other nationwide builders, and they will have a component list of prices. You want a covered porch on the back of your house, they can add it for a set price of $4,500.

LARS: And you’ll have that info?

THOMAS: I try to get it if at all possible. I search out every form of data I can get my hands on. We don’t just use national cost manuals, we also use local cost sources like building supply and lumber stores, and other local market data too. Any national cost data that you get, you have to localize it to your particular market, because lumber, transportation, permitting, and labor costs can vary so much.

LARS: And from year to year?

THOMAS: Yes. Costs can definitely change from year to year.

LARS: So I’ve got the cost tables, those are frozen, I don’t have any degrees of freedom there, I just have to follow the rules. I’m going through, I’m punching them into the CAMA. What else am I doing as a junior appraiser to the point where you can feel comfortable letting me do it by myself?

THOMAS: You want to identify if there are differences in home prices in a development. If there are differences, why do they affect certain houses? Is it a difference in the lot size, quality of construction, foundation type? Some developers charge a “lot premium” for different things like a better view a golf course or proximity to the neighborhood pool or some other amenity.

LARS: And so what is the action I’m taking to make the pieces fit?

THOMAS: First, you determine what caused a difference in price, then you check and see if there are similar properties in that neighborhood that might be affected by that same condition. If there are, compare those properties with others that do not have the same condition. This is what we call “matched pairs analysis”. In theory, any difference in value can be attributed to the physical differences between any two properties. Because house types and lots are typically very similar in tract neighborhoods, it is relatively easy to isolate the different components to derive your adjustments.

LARS: Okay, so what that sounds like to me is I’m creating some tables, right? I’m creating maybe like a base value, and then I’m creating some adjustment values for certain cases and defining those?

THOMAS: Possibly, yes. If you can do that in your CAMA system or whatever that you are analyzing. We always have to remember, at least in North Carolina, everything that’s in there has to be made public. We have to be transparent and we have to be equitable.

LARS: So not just those three line items on the public card, but all my scribbles, everything.

THOMAS: Every table is made public. Every county has to publish what’s called a schedule of values, which outlines how your property is valued.

LARS: So if I have “Lars’s dirty hack to make the numbers work,” in there?

THOMAS: You probably wouldn’t want to do something like that. There has to be a way for the public to be able to see how the county calculated your value. When I was in private practice, one of the ways we would successfully challenge an assessed value is if the county utilized unpublished adjustment tables. If a county used adjustment tables or ranges that were not at least referenced in the schedule of values, it was easy to make the case that the undisclosed adjustment was likely arbitrary and a violation of state tax law.

Level 1

LARS: Let’s treat this a little bit like a video game where you start on level one and everything’s real simple and then you add one more thing at a time.

So let’s say I have my neighborhood of tract homes. I’ve got all the cost figured out, all the depreciation. I’ve tagged everything that has a view, I’ve figured out which lots are weird shapes, which ones have excess land or surplus land. I’ve got the zoning ordinance and all that context figured out. I haven’t punched in land values yet, but as far as I can tell I’ve controlled for everything but that. At this point is the difference the land value? I need to make it rise so that when I add it to my cost plus all the other stuff, that I get within acceptable tolerance of the sale prices?

THOMAS: In theory, yes, it is.

LARS: Now, do I just need to make it rise so that when I add it to my cost plus all that other stuff, that I get with an acceptable tolerance to the sale prices?

THOMAS: According to the theory, the sales price minus the depreciated value of the improvements, the remainder is going to be the land value.

LARS: So in a totally homogeneous neighborhood, with all the land the same size and shape and zoning, and all the homes built within, say, five years of each other, and they’re all more or less identical, does pinning down a base lot value get you to the end of “level one?”

THOMAS: Every appraiser wishes that the majority of the subdivisions they analyze are this homogeneous and straightforward. In theory, like I said, it should be very easy to figure out the land value in this type of development.

Level 2

LARS: What’s a complication you add that makes it a little harder?

THOMAS: I’ve run into instances where the county or the state had announced they were going to construct a four-lane road highway adjacent to an existing subdivision. Up until the date that the construction project was announced to the public, the prices of homes and undeveloped lots were consistent throughout the subdivision. After that date, the prices of homes and vacant lots on one side of the street went down $10,000 to $15,000. The proposed road had not been added to the county GIS yet so there was nothing that stood out as to why the sudden difference in sale prices. I was flummoxed so I did what everybody else does, I went to Google and entered the name of the subdivision, the street name in the subdivision, and the main public road at the entrance to the subdivision. Google returned a bunch of news articles announcing the new highway and the 20-foot sound deflecting wall that would run along all the houses bordering the new road. Other times I’ve seen sewage assessments that affect a small subset of houses within a larger development. These things do happen and you do your best to find out what’s going on. It’s like solving a mystery. There are a million different things that pop up like that, sometimes the only way you can figure it out is experience.

Level 3

LARS: What’s another?

THOMAS: You’ve got cases like in Silicon Valley, where you have a 1973, 2,800 square foot brick ranch—that same house might go for $250,000 somewhere in North Carolina. In California it’s $3 million. That’s location specific. It doesn’t have any correlation to the actual cost to build that house.

LARS: So is the difference between the North Carolina home and the California home, I mean, is that just land value premium because of the location?

THOMAS: It very well could be a location premium. It’s definitely a function of supply and demand, and this is not uncommon in other local markets either. There’s always a hot area where somebody wants to live or build.

LARS: The bigger that locational premium is, I figure the easier it is to notice it? As opposed to when the location premium is low, it’s kind of hard to separate.

THOMAS: Generally, it is. Where it can be difficult is when you’ve got adjacent areas that are closer to that high demand area. Redevelopment hasn’t quite crept out there yet, but asking prices already have.

LARS: So this was something I saw just in my own research the other day. I was working on a report for Maryland. And I noticed something—I was looking at the Bethesda neighborhood, which is kind of an upscale place. And I noticed this weirdness while I was validating vacant land sales, I noticed there were vacant land sales there, and they were going for a value that was lower than the improved sales, which is normal. But then I noticed some improved sales that were going for the same price as the vacant land sales. And I noticed they were all homes from the 1930s that were a third as large as all the new buildings.

THOMAS: And that’s the functional obsolescence that we talked about. If the existing house is below current market expectations, Is it curable? Can you add a third bedroom and a second bathroom to the structure to make it more palatable to potential buyers. If not, or if the cost to do so is too high, then the improvements might not have any contributory value.

LARS: What was interesting is that the market seemed to be pricing these things as the building basically being worth zero.

THOMAS: Yep. And that is a clue in itself. When the improvements are trending below the land value or approaching zero, that means the highest and best use is changing or the existing houses may be under improvements for that particular market. And that’s suitable for redevelopment then. That’s, that’s the big clue.

LARS: So, when you see a neighborhood, which has two kinds of building typologies and the older and smaller building typology is not selling for any more than bare sites, then that indicates that the market sees these as tear-downs?

THOMAS: I had a case recently, where a residential property owner purchased an older home that was adjacent to several commercial properties. The property was zoned as commercial, but the residential use was also permitted. The homeowners completely renovated the property and moved into it. When the property was reassessed last year, the residence itself was fully taxed as if it were a residential structure, in like new condition with a very low effective age. The county tax office also valued the land as if it were commercial use, compatible with its zoning. The renovated house might have been considered an under improvement for that lot, but the value of the land indicated a change in the highest and best use. This is not an uncommon occurrence, but it violates the Theory of Consistent use, meaning that the land and the improvements must be valued based on the same highest and best use.

You cannot value the land as though it will be used for one purpose, while also valuing the existing building as though it will remain in another use.

LARS: I see.

THOMAS: If you’re saying the highest and best use of the land is commercial, then the residential improvements have zero value.

LARS: So if you’re going to say that it’s commercial land, which is plausible because it’s zoned commercial and the market might buy that—but if you’re making that argument, the incompatible residential use is contributing nothing to that commercial value.

THOMAS: Exactly. So the county can’t have it both ways and cherry pick the highest value of each, because then you’re overtaxing the citizen in that case.

LARS: What it can’t do is basically create a layer cake of half one and half the other.

THOMAS: Exactly.

LARS: What it can do is say: here’s residential land valuation and residential building valuation, that would be this residential total value. And then, here’s commercial land valuation and commercial building valuation, and in this case the “commercial” building valuation is zero because it’s a residential home.

THOMAS: That’s right. Unless the house could legally be renovated into leasable office space, and if there’s a market for a renovated house as office space, then it could conceivably be converted to commercial use, but it has to be worth it to do so.

LARS: That’s what they would have to defend.

THOMAS: Yes, but fortunately for the homeowner, the county couldn’t defend their valuation, and the land value was reduced.

Final Boss

LARS: So going back to our little video game metaphor, what’s the final boss?

THOMAS: It’s data quality. Always. That’s the bane of every tax office, of every appraiser.

LARS: Is it lack of sales or lack of characteristics?

THOMAS: Generally, it’s lack of sales. You have to compare it with something. And in appraisal theory, if you don’t have sufficient sales in an area, you can either go back in time or you can extend your search area outward to try to find a comparable neighborhood or comparable property. Sometimes that’s easier said than done when you’re doing mass appraisal, because in a lot of tax offices, they like to stay within the jurisdiction of the county. They don’t want to go back in time prior to the previous revaluation. So you might be dealing with three or four years of sales in the county, and especially for commercial properties, you might not have had a sale of a unique property type within that time frame within the county. So you might have to search several counties over or throughout the state to try to find meaningful data.

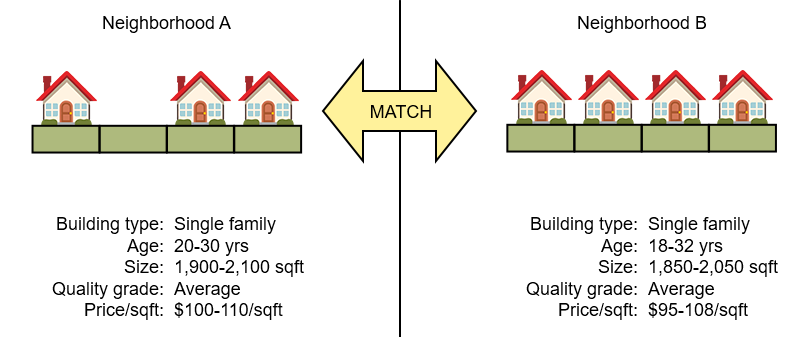

LARS: Let’s keep it residential for now. Let’s say you’ve got a residential neighborhood and you just don’t have any sales in it, and you go back in time and there’s none recently. But you have another neighborhood that has the same kind of typology. It’s got similar land shapes and sizes and similar building sizes, types, and ages. And you notice you don’t have any land sales in neighborhood A. But in neighborhood B, you do have land sales. And you notice that these neighborhoods have similar selling prices for houses overall. Is it fair to assume they have comparable land values on the neighborhood level?

THOMAS: Yes. If that neighborhood has characteristics similar to one you are evaluating.

Open Data

LARS: So in theory, maybe I have to write some data record requests, but I should be able to go to any North Carolina county and say, can I see your tables and see if I can reproduce all your results?

THOMAS: Yes. Counties should be able to supply you with copies of any tables that were used to value any property. As I stated before, they are typically published in the Schedule of Values, and most counties have copies of those online. If cost ranges were used in the schedule of values instead of a complete table, then you can again request a copy of the complete table that is referenced in the schedule. Sometimes the online representation of what you see as your value is not the complete picture. I always recommend that taxpayers request the actual tax card to be printed out, not just what’s on the web page. The actual tax card will show data from the CAMA system and detail every adjustment that’s made.

LARS: Can you request that in bulk?

THOMAS: I don’t see why not. You might have to pay for printing costs, which would be substantial or typically you can request the information in digital format as an Excel or .CSV file. Most larger counties in North Carolina have most of this information available as a data file on either the tax website or the county GIS website for free.

LARS: Right.

Land as an Afterthought

LARS: Now, I’ve worked with a bunch of different jurisdictions, a bunch of different places, and some places struggle more with land than others, and my goal is just to help everybody learn from the best. And I’ve seen some places where land is sometimes—to kind of be polite—it’s kind of an afterthought. Because we’re taxing on the total value, and there’s no law that really cares about the land value, and so what will sometimes happen is they’ll just do the land as an afterthought, they’ll write something, anything down.

And one thing I’ve seen sometimes is that they will just do an allocation, but the way they’ll do the allocation is per parcel. They’ll have their total market value, and they’ll just be like, okay, the land is, say, 20% of whatever the total market value is.

THOMAS: You have to be careful when you’re doing something like that. If they are trying to just match the sale price, but the land is essentially identical, then this might be masking a feature or condition that has not been picked up by the appraiser. This is especially true for residential properties. Commercial properties might be different if they are income producing and the total value is based on the Income Approach. In my opinion, when residential land is valued this way, it would be much harder if not impossible to defend during an appeal by the taxpayer. It doesn’t make sense that identical lots in the same subdivision or neighborhood would have different values, and if I were a taxpayer, that is the first bit of evidence I would bring up in an appeal.

LARS: What should you do instead in that scenario? What’s the least you can do?

THOMAS: First thing is that I would review the tax cards for all the sales to try and find if the differences in sales prices are anything more than normal variances. There is so much information available on the web including Zillow, Redfin, the local MLS if available, to make sure that what is recorded on the parcel card is correct. Once I did that I would look at my available data to determine which types of analysis I can perform to try and accurately determine the land value. If you have enough improved sales you can utilize the Extraction method where you start with an improved sale and subtract the depreciated value of the improvements to isolate the land value. Like you mentioned, the Allocation method can be used but one of its greatest weaknesses is that it depends heavily on a reliable land-to-building relationship. It’s usually better suited for broad reasonableness checks than for highly precise valuation. If you can find rental information, including current income and expense data, you could possibly use the land residual method. This is an income-based method which estimates the income left over to the land after the improvements receive their required return. With so many residential properties being purchased as AirBnB rentals, data is readily available and can be supplemented with occupancy tax data if it is levied in that city or jurisdiction. Basically, you use whatever appropriate appraisal methodology you have the data for. If possible, perform multiple types of analysis and compare the results to test for reasonableness, then you decide what is the best fit.

LARS: Is it appropriate to say that all else equal, if two side-by-side lots, all the land characteristics, location, and all the characteristics, like size and shape and grading of the land is the same, regardless of the improvements, should they have the same land value?

THOMAS: Yes.

LARS: Because it would require a different characteristic, legal use, et cetera, to justify a different land value, right?

THOMAS: Correct.

LARS: So what is a way to recognize and test when land values are good?

THOMAS: If you see an assessed value that is greatly above or below an acceptable threshold for that land, or if you see what builders are paying for land and the tax value doesn’t reflect the market, then you know somewhere you’re off. As I stated previously, depending on the available data, you can perform other types of analysis besides Allocation. It’s really just a test of reasonableness. When I was taking my first appraisal courses 30 years ago, my instructor always said, “Before you sign off on any value, stop and ask yourself, what would you yourself actually pay for this property?” This goes for both vacant and improved properties. Then ask, “What would a typical person or typical investor pay for the same property?” If there is a difference between the two, you should take another look at your value.

LARS: And you’ve already talked about uniformity is another test.

THOMAS: Correct.

LARS: Thank you very much, Thomas. I really appreciate it. Where can people learn more about your work?

THOMAS: They can come to our website, pinerappraisal.co. We have our contact information on there. You can see the services that we offer.

“Fee appraisal” refers to the practice of valuing one property at a time. This is most commonly done for business transactions, legal cases, and mortgage lending. “Fee appraisal” differs from “Mass appraisal,” which is valuing many properties at once (what your local property tax assessor’s office performs). For more on this distinction, see Mass Appraisal for the Masses.

“Tax office” is assessor jargon for a state or local government property assessment office, which values property for property tax purposes. This is almost always done using mass appraisal.

CAMA: Computer Aided Mass Appraisal. Essentially a glorified database with appraisal functions attached.

The “four factors” of production Thomas is referring to here are Land, Labor, Capital, and Entrepreneurship, under the neoclassical four-factor model.