Under what circumstances is the payment of land rent a tax?

We first need to consider land rent in a pure market economy. The rent is collected and divided equally in cash. The purchase price of land is near zero. The rent is based on the benefits of that location and extent of space. Therefore, in such a pure case, the rent is not a tax, as it is just another price paid for the use of land, and on average, people get back what they pay.

Now consider a zero-tax economy in which a land title holder has all rights to a plot of land, including its rent. As land rent captures the gains from economic expansion, rent and land value rise. The payment of rent is still not a tax, because the higher rent reflects the greater productivity of the location. With no taxes, the landowner must pay for the works that service the land, such as streets and roads, security, fire protection, and utilities.

After these expenses, suppose some of the site rental is left as profit. As these profits rise, land values rise, and land speculators jump in to flip properties - to buy, hold, and then sell at a higher price. As the purchase price of land removes those of lower income and uncertain credit from buying land, they become renters, and the rent rises even more. This rent increase due to the speculative rise in land values is a tax, as the higher rental is not matched by greater locational services.

Now consider an economy in which taxes are only on wages. Now the landowners do not pay for public works, as they are financed from taxes on labor. The higher rent generated by public works is an implicit subsidy to landowners, which induces even greater land speculation. The higher rent due to the subsidized speculation is a tax.

Therefore, rent becomes a tax when there is an increase due to land speculation, especially when the rent is an implicit subsidy from public works paid from taxes other than on land value.

Land rent fell during the recession of 2008-2009, as the land speculation boom crashed. After the vacancies were filled and economies world-wide recovered, rent rose again. As land values have risen to match previous highs, rent has risen also, and the portion of household income going to housing has risen. As rent increases faster than wages, much of the increase in land rent is a tax due to the implicit redistribution of wealth from worker-tenants to landowners.

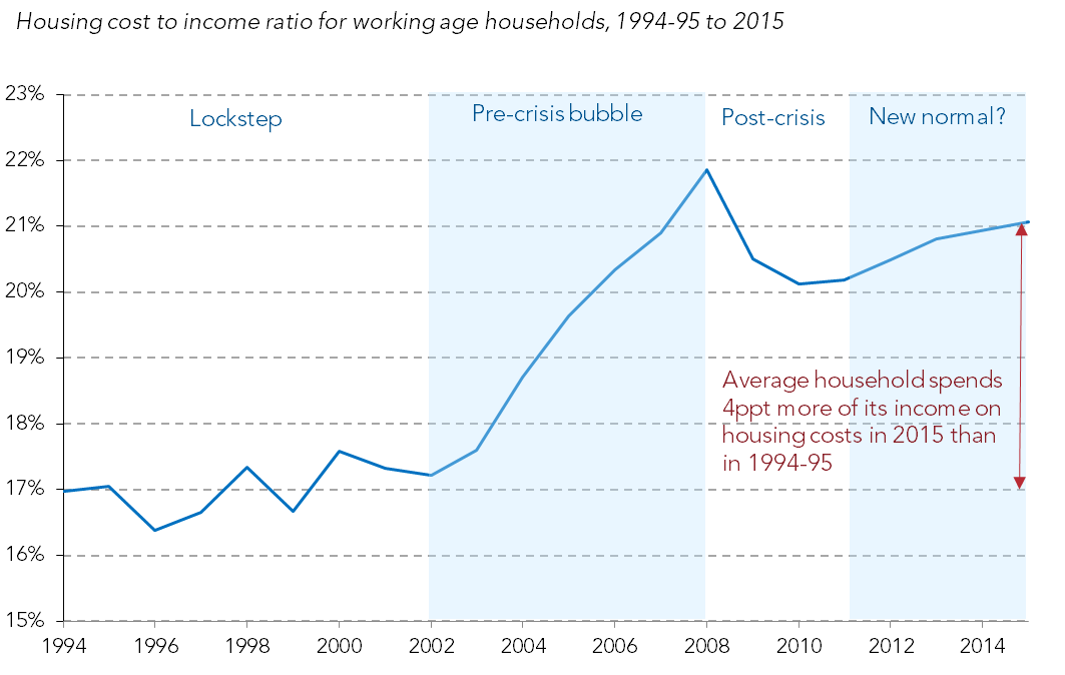

An article by the Resolution Foundation of the UK, published on 26 April 2016, has the title, “Rising housing costs since the 1990s equivalent to 10p [10 pence] increase in basic rate of tax for a typical family.” The story was similarly published by the Financial Times. From 1995 to 2015, the portion of family income paid for rent rose by 4 percent. A similar increase in the portion of income paid as rent rose in the USA.

US renters paid 21% of median household income for the median monthly rent of $934 in 2014. This is the highest fraction of median household income going to housing since such data began to be calculated in 2005. The California Median Gross Rent in 2014 was $1,268, a 5% increase during the previous 3 years, with 25% of median income going to housing.

The old rule in the US housing market was that a household should not pay more than 30% of its income to housing. In the USA, median rent rose by 4% from 2001 to 2012. Some 35% of households spend more than 30% of their income for housing. One fifth spend more than half their income on housing, according to the Joint Center for Housing Studies of Harvard University. Many of the poor in the USA obtain housing subsidies, but then the landlords raise the rental, since the tenant can now afford to pay more.

Some cities respond with rent control, but government cannot control land rent. Government can only control who receives the rent. If the landlord does not obtain the rent, then in effect, the tenant is keeping what would have been paid, and is obtaining an implicit rent. While some tenants benefit from the rental-recipient control, others are locked out of housing.

If we roughly figure the difference between the rentals in California and that of the USA as being due to greater governmental intervention both in land use and in fiscal policy, then Californians are paying an extra 3% of their income as the rent tax. California does have a favorable natural climate, and that generates higher land rent, but that would not need to create higher housing costs if land-use rules allowed for more construction and density to match the greater demand, and if excessive speculation were not driving up the rent.

The only way to avoid rent as taxation is to avoid the excessive land speculation by collecting the land rent and distributing it as either cash or public goods.